TL;DR: Agentic commerce is real, but extremely early. Sales impact today is small and unclear, and most brands and retailers are testing around it rather than betting big. Optimize product content so agents can read it, experiment thoughtfully, and monitor evolving business models, but don’t lose sight of initiatives with clearer near-term ROI while the channel matures.

8 minute read

Agentic commerce is everywhere right now. Every conference, every investor deck, every panel, every C-suite discussion.

What’s harder to find is an honest account of where things actually stand.

This report provides one.

Over the past few weeks, we combed through earnings calls, conference presentations, public statements from brands, retailers, and platforms, and heard directly from retail leaders across the eCommerce ecosystem to separate the signal from the noise.

Our research indicates it’s earlier than the hype suggests, the sales impact is either small or unmeasured, and the companies closest to it are mostly testing and hedging, rather than making agentic commerce their top priority. This isn’t a pessimistic take. Rather, it’s the honest baseline from which smart decisions can be made.

Here’s our analysis of where agentic stands inside brands, Amazon, Walmart, Instacart, and Shopify, and what we think it means.

CPG Brands Didn’t Share Much

The most revealing thing about agentic commerce at the Consumer Analyst Group of New York (CAGNY) conference wasn’t what brands said, but rather what they didn’t say.

Of 31 large CPG organizations presenting their strategies to investors and industry stakeholders, fewer than 10% addressed agentic commerce in any meaningful way.

The three companies that did speak were worth listening to, even if what was said was unsurprising. General Mills kept it high-level, framing agentic as simply another evolution of eCommerce discovery. McCormick was more concrete, focusing its preparation on ensuring its data stack is ready to interact with and influence agents. L’Oreal went furthest, describing a direct data partnership with ChatGPT: “We load our own data directly into ChatGPT so that they don’t have to scrape and we can make sure that it’s the kind of data that the consumer is looking for, (similar to our) partnerships with Target and Amazon on those same kinds of topics.”

That L’Oreal quote is worth pausing on. Proactively feeding structured data to ChatGPT, rather than waiting for it to scrape whatever it finds, is one of the few concrete, executable actions a brand can take today. The fact that only one company out of 31 mentioned anything like it tells you how early this actually is.

Across the board, CPG brands at CAGNY were far more focused on using AI to accelerate internal capabilities than on preparing for agentic commerce as a consumer-facing channel. For the companies that do want to get ahead of it, the consistent theme was data readiness, ensuring their product information is structured, accurate, and machine-readable. While this is not the sexiest of investments, it’s the right foundation, and notably, it wasn’t a top priority for the vast majority of the presenting brands.

Amazon’s Rufus Contributed $12 Billion, Search $870 Billion

Amazon is the leading vertical agent in the space, and its Rufus chatbot is the most useful barometer we have for agentic commerce adoption. It’s the only chatbot trained on Amazon’s full product catalogue and consumer data, backed by the largest Prime customer base in the world. If agentic is going to move the needle anywhere, it should show up here first.

So far, the numbers are impressive-sounding in a vacuum and modest when compared to Amazon’s scale.

Amazon reported that Rufus was used by 300 million+ customers and generated nearly $12 billion in incremental annualized sales in 2025. Importantly, Amazon didn’t disclose its methodology, and as a company with real incentive to make chatbot ROI look compelling to nervous investors, it’s inclined to report the largest defensible figure. Taking them at their word, $12 billion is approximately 1% of total GMV. Even if it doubles in 2026, it’s a rounding error for Amazon.

That sales level explains something brands have been quietly frustrated by: even those who’ve done the work to optimize their PDPs for Rufus can’t tell if it’s helping. And that’s not entirely their fault. Retailers and LLMs return almost no meaningful data to brands. Search algorithms were always somewhat of a black box, but LLMs are black holes. You can put things in. Little if anything measurable comes back out.

Third-party tools are emerging to help brands understand how they’re showing up in chat results, but their methodologies are still being scrutinized and their accuracy questioned. The measurement problem is real, and it isn’t going away soon.

None of this means brands should ignore Rufus. It means they should reframe what Rufus optimization is actually for.

The goal isn’t to drive direct sales through Rufus. The goal is to be contextually relevant on Amazon, full stop. PDPs optimized for COSMO and Rufus-related elements, like addressing real customer questions, improve organic rank, conversion, and media efficiency across every mechanism a consumer uses to search and discover, not just chat. In other words, you don’t need mass Rufus adoption to justify updated, optimized product content. You need it because it supports both the $12 billion in Rufus-related sales and the roughly $800 billion-plus that Amazon generates in “non-Rufus” sales.

That’s a much easier business case to make and a more justifiable reason to act.

Walmart’s Hedging with Vertical & Horizontal Agents

Walmart is doing something interesting that Amazon isn’t: it’s hedging in both directions. It has Sparky, its own vertical agent built into the app, while simultaneously partnering with ChatGPT and Google, the horizontal agents Amazon has been openly skeptical of. This dual approach shows Walmart doesn’t know which way the consumer is going to go, so it’s covering both bets.

The optimism from Walmart’s leadership is genuine. Sparky, they say, is moving the company from keyword search to intent-driven commerce, understanding whether a shopper is planning a camping trip or a birthday party and building a shopping solution around that. Roughly half of app users have tried it, and customers who use Sparky show an average order value about 35% higher than those who don’t. Like Amazon’s 300 million-plus Rufus users, those are meaningful engagement numbers.

What Walmart didn’t say is equally meaningful. There was no disclosure of direct sales impact from Sparky, and no detail on the traffic or conversion lift from its ChatGPT and Google partnerships. That silence suggests the actual revenue impact is still small and that those external partnerships are test-and-learns rather than long-term strategic commitments.

The implication for brands mirrors what we said about Amazon. Get your product content optimized and machine-readable so Sparky can work with it. But don’t build a financial case around Sparky-driven sales yet. That case doesn’t exist in the data, and Walmart isn’t saying it does.

Instacart Says it’s Very, Very Early

Of all the companies we heard from, Instacart may be the most honest about where agentic commerce actually stands, which is saying something, given how much it has invested in getting there first.

Instacart was the first grocery platform to launch native checkout directly inside ChatGPT. It has partnerships with OpenAI, Google, and Microsoft. Its former CEO now runs Applications at OpenAI. If any company had reason to talk up the commercial reality of agentic commerce, it’s Instacart. And yet its leadership said it’s not material.

Not “early but promising.” Not “tracking ahead of expectations.” Simply, not material.

It’s worth sitting with this for a moment. A company that is better positioned than almost anyone to benefit from agentic commerce becoming a real sales channel is telling investors, plainly, that its agentic efforts to-date aren’t moving the needle. Consumer behavior, they acknowledged, is likely to shift, but it’s “still very, very early.”

So what is Instacart actually doing? Exactly what the honest answer to “very, very early” demands: building infrastructure, securing partnerships, and ensuring it’s discoverable if consumers eventually decide to shop there in a greater way, all with a goal towards figuring out how to migrate consumers it wins agentically to its own app later.

For brands, Instacart’s candor is telling you directly that 2026 is not the year to build your business case around agentic grocery commerce. It is the year to run small tests, ask Instacart for whatever data it can share on how these partnerships are influencing the business, and stay close enough to move if the picture changes.

The companies that will be best positioned as agentic evolves aren’t the ones making big bets now. They’re the ones who are staying curious and lean, and don’t mistake partnership announcements for progress.

Shopify’s Merit-Based Shopping is a Myth

Shopify shared the most bullish view in this report, and also the one that requires the most scrutiny.

Its pitch is compelling on its face. Shopify powers thousands of DTC merchants, from small independents to global brands, and it wants every one of them discoverable inside every major AI platform including ChatGPT, Gemini, Microsoft Copilot. Its Agentic Storefronts product syndicates billions of products across those platforms. Orders to Shopify stores from AI search are up 15x since January 2025. Its CEO declared, flatly, that “the AI era has now reached commerce.”

Its enthusiasm is real, and so are its incentives to promote it.

Shopify’s business model depends on its merchants believing the next wave of commerce runs through Shopify infrastructure. Of course it wants to be, in its own words, “at the center of everything happening when it comes to Agentic Commerce.” But that doesn’t mean agentic is inevitable, and it’s important context to evaluating its data like referral traffic from agents rose 15x for its DTC clients, which was shared without a denominator.

Shopify’s leadership has framed agentic as “merit-based discovery at scale”, meaning the idea that AI agents, scanning the whole web, will surface the objectively “best” product for every consumer, free from the distortions of advertising and algorithmic bias. It’s an appealing idea, but also fundamentally flawed.

ChatGPT is already running (expensive) ads and charging commissions. The same dynamics that turned Google search, Amazon’s marketplace, and Meta’s feed into pay-to-play environments will apply here too, because they must. OpenAI has investors, and that means it needs returns, and therefore will have all the same inclinations as its predecessor tech companies. Paid subscriptions have never been enough for a consumer internet business model. The more traction its agentic commerce offering gets, the more valuable placement inside it becomes, and the more OpenAI will charge for that placement. There’s no version of this that ends with a free, objective, merit-based shopping layer sitting on top of the internet. That’s not how any of this has ever worked.

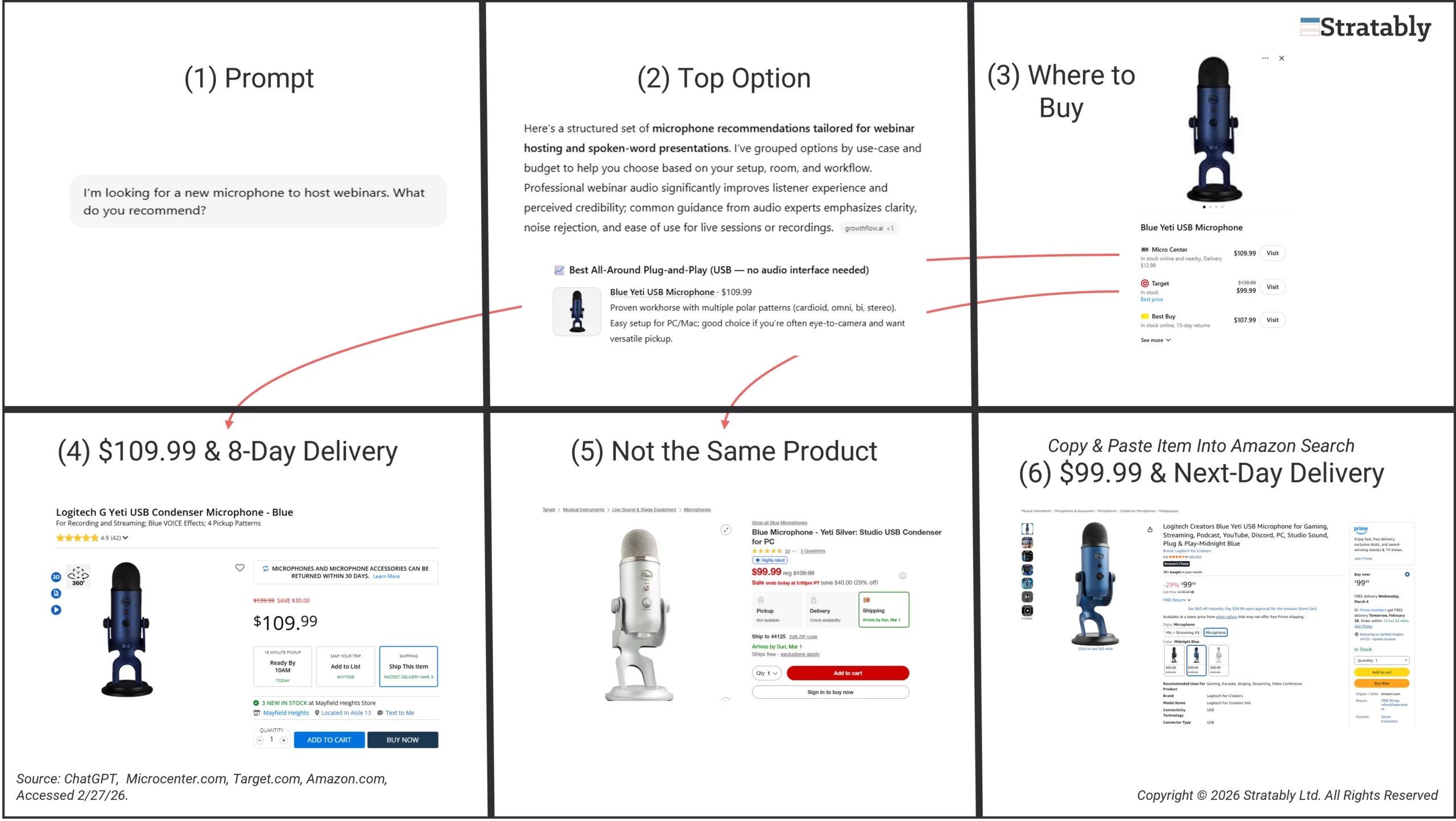

In addition, these horizontal agents don’t have partnerships with Amazon, meaning they’re offering products often at higher prices and worse delivery than Amazon, as the graphic below illustrates.

Surfacing a microphone from MicroCenter for $109.99 and 8-day delivery is inferior to simply buying it on Amazon for $99.99 with next-day delivery. It seems unlikely in a value-driven environment that consumers will put up with higher prices and slower delivery. If they know and trust Amazon, they’re a copy and paste away from simply buying it there, not altogether different than what they do with TikTok-discovered items or how they went from researching on Google to buying on Amazon.

The key question for OpenAI is how many of these consumer experiences will a shopper put up with before trust is broken?

For brands on Shopify, the practical implication is straightforward: make sure your product data is structured so Shopify’s Agentic Storefronts can do its job. But don’t let Shopify’s conviction about the destination distract from the uncertainty of the timeline or even the likelihood that when agentic commerce does scale, it will look a lot more like the ad-supported ecosystems we already know than the merit-based utopia being promised.

Russ’s Final Thought

Nobody knows where this goes. Not the consultants selling certainty about it. Not the retailers investing in it, nor their AI partners. And to be fair, not us! Even Sam Altman doesn’t seem to be all that certain.

What we do know: consumers are unpredictable, the technology is moving fast, and a wholesale strategic pivot right now would be premature. The hand-wringing is a waste of time. So are the dramatic LinkedIn hooks.

Relative to peers, our research suggests you’re in a good spot as we sit here in March 2026 if you’re:

- Studying

- Experimenting

- Testing and learning

- Trialing new agentic share tools launching

- Seeing how chatbots evolve their business models

- Watching what partnerships retailers form (or don’t form)

- Working through organizational silos to designate a team to work on it

- Developing a sound financial business case to support agentic commerce investments

In other words, taking a balanced approach.

Nearly every brand we work with has multiple, competing priorities. They have to make tough choices. They face opportunity costs. Initiatives to improve profitability on Amazon are important, new investments needed to gain share inside of Walmart’s stores are important, beginning to advertise on DoorDash is important, launching on TikTok Shop is important.

Agentic commerce is important too. It’s probably at the top of your test & learn program. But it probably shouldn’t be at the top of your overall priorities if you have numerous other initiatives that have clearer paybacks enabling the organization to hit their top and bottom line goals.