May 22, 2024

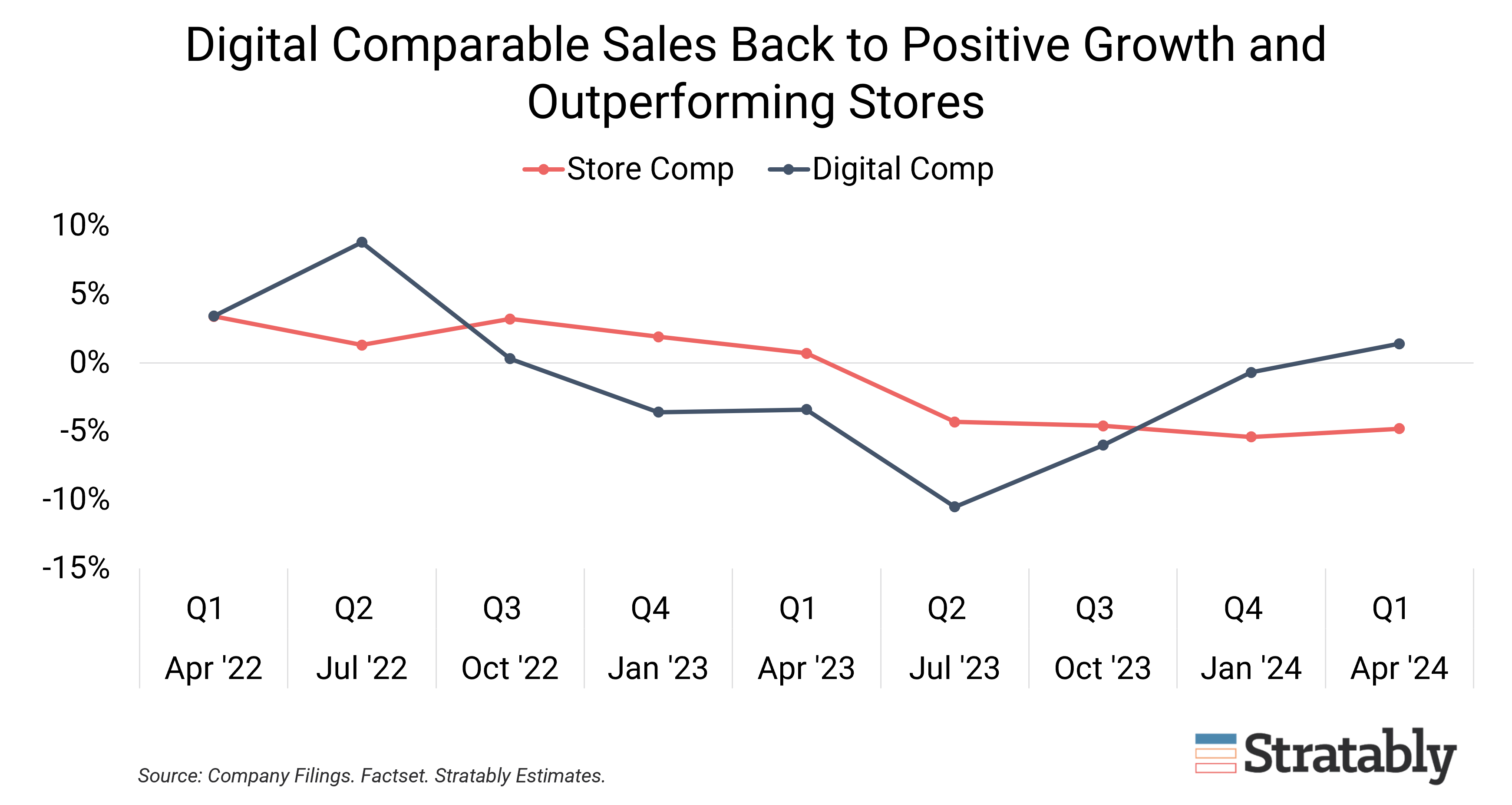

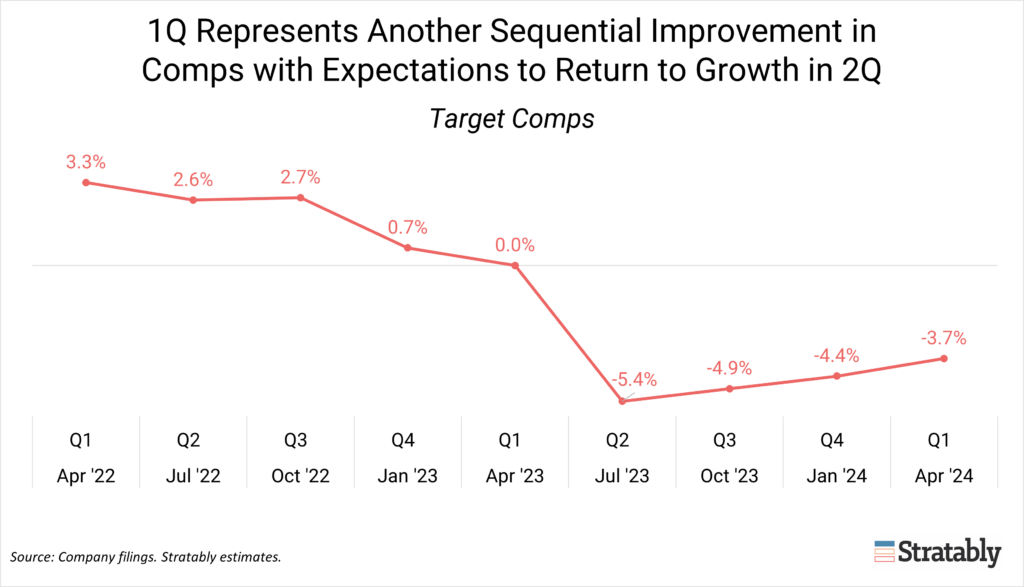

This morning Target reported another quarter of sequential improvement in declining comps (down -3.7%) as softness in discretionary categories continues to ease. Digital turned the corner into positive comparable sales territory (+1.4%) to offset mid-single-digit declines (-4.8%) in the stores business.

The company expects to return to positive growth in 2Q, with investments into newness and value, and easier comps, the key drivers.

Read on for a summary of the results, with a special focus on what digital leaders need to know.